August 18, 2025

This is the Recycling, Scrap Metal, Commodities and Economic Report, August 18th, 2025.

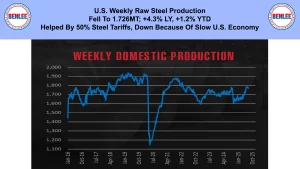

U.S. weekly raw steel production fell to 1.726MT up 4.3% from last year and up 1.2% year to date. Production was helped by the 50% steel tariffs, but down because of the slow U.S. economy.

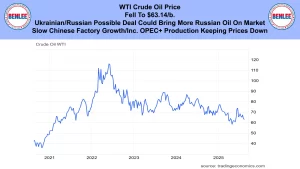

WTI crude oil price fell to $63.14/b. as a Ukrainian Russian possible deal would bring more Russian oil on the market. Also, on slow Chinese factory growth and increased OPEC+ production keeping prices low.

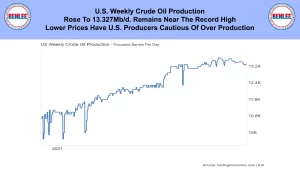

U.S. weekly crude oil production rose to 13.327Mb/d. which remains near the record high. Lower prices have U.S. producers cautious of over production.

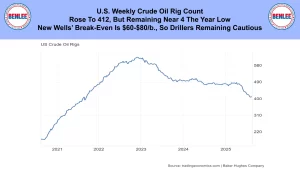

The U.S. weekly crude oil rig count rose to 412 but remaining near the 4 year low. New wells’ break-even is about $60-$80/b., so drillers are cautious.

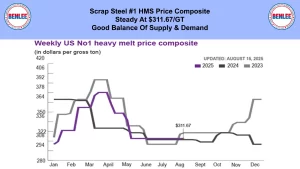

Scrap steel #1 HMS price composite was steady at $311.67/GT on a good balance of supply and demand.

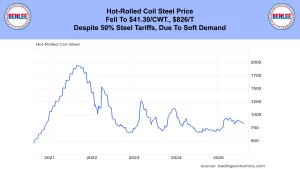

Hot-Rolled coil steel price fell to $41.30/cwt., $826/T. despite the 50% steel tariffs, due to soft demand.

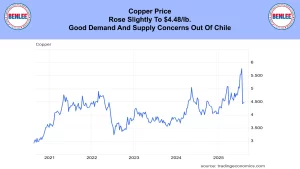

Copper price rose slightly to $4.48/lb., on good demand and supply concerns out of Chile.

Aluminum price fell slightly to $1.18.lb., which is $2,604/MT on lower supply, but lower demand.

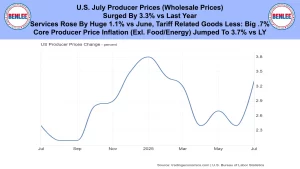

U.S. July producer prices as in wholesale prices surged by 3.3% vs last year. Services rose by a huge 1.1% vs June, but tariff related goods rose less at yet still a big .7% for the month. Core producer price inflation, which excludes volatile food and energy, jumped to 3.7% vs last year.

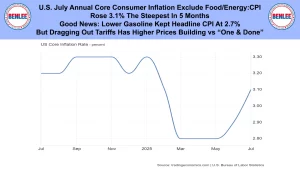

U.S. July annual core consumer inflation, excluding again volatile food and energy inflation, also called CPI. It rose 3.1%, the steepest level in 5 months. The good news is lower gasoline prices kept headline CPI at 2.7%, but dragging out tariffs has higher prices building, vs a one and done.

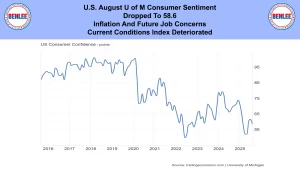

U.S. August U of M consumer sentiment dropped to 58.6 as there were inflation and future job concerns. Also, the current conditions index deteriorated.

U.S. July retail sales were slower at 3.9% vs last year. Motor vehicles and furniture grew the most.

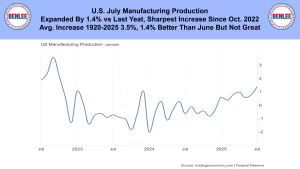

U.S. July manufacturing production expanded by 1.4% vs last year, the sharpest increase since October 2022. But he average increase from 1920-2025 was 3.5%, so 1.4% is better than June, but not great.

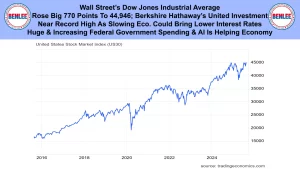

Wall Street’s Dow Jones Industrial Average rose 770 points to 44,946 on Berkshire Hathaway’s United Health investment. The market is near a record high as the slowing economy could mean lower interest rates. Note that huge and increasing federal government spending and AI is helping the economy.

This is Greg Brown. As always, feel free to call or email me with any questions, and we hope all have a safe and profitable week.